no exam life insurance

Pros

Get your policy issued quicker without the hassle of an exam

Cons

No Med Life Insurance can sometimes be a little more expensive

Advice

Always compare No Exam policies- they vary in price and approval times

The American Amicable Life Insurance Company of Texas can trace its roots all the way back to 1910. They are a progressive market insurer. American Amicable offers both annuity and life insurance products.

Their products have been developed in order to target the needs of wealth creation, protection and preservation of estate. American Amicable continues to prosper and grow.

They have consistently provided and maintained solid finances. American Amicable (part of the American Amicable Group) was acquired by Industrial Alliance Insurance and Financial Services, Inc. in the year 2010. American Amicable is looking toward the future with enthusiasm. They have a history of responsible management, financial integrity, and a strong commitment to their policyholders.

American Amicable Tip – If you pay an annual premium you will save almost and entire 1 month of your premium every year.

Founded in 1905, ANICO (American National Insurance Company) has been insuring more than five million Americans. American National is located in Galveston, Texas. They are over a century old. This means they are a life insurance company that you can count on now and in the years to come.

ANICO is an “A” rated (Excellent) for their financial strength by AM Best Company (As of September 4, 2015). The American National Insurance Company offers a wide variety of life insurance products including term life insurance and whole life insurance. They are well known for their no exam life insurance plans.

American National Tip – American National provides a great opportunity for those who need some wiggle room with underwriting. They are great choice for some high risk health situations such as tobacco users, diabetics and other health conditions.

Read our review of American National ANICO

Started in 1890, Assurity has a mission of helping people through times of difficulty. Assurity provides disability, life insurance, as well as critical illness insurance. They also provide voluntary employee benefits through nationwide independent brokers. Assurity’s commitment is unrelenting.

Their financial strength and stability has consistently earned them excellent ratings throughout the industry. Assurity is a mutual organization, which is important to know. It means they have no publicly-traded stock or shareholders. That means that their policyholders share in the company’s ownership. Ultimately, it means Assurity is in business to serve the interests of their policyholders.

Assurity Tip – If you pay an annual premium you will save almost and entire 1 month of your premium every year.

Read our full review of Assurity

Banner Life remains the company that underwrites and issues our life insurance policies. However, we represent the market under a single name, Legal & General America. Legal & General began over 178 years ago in 1836. That is when six lawyers would meet in a London coffee house. The topic of discussion?

Life insurance of course. These men decided to put together an association under the chairmanship of John Adams. This was eventually named Legal & General Life Assurance Society. Legal & General has over 10 million customers currently. These customers have trusted Legal & General for their life insurance, pensions, investments and general insurance plans.

Banner Tip – Banner Life provides underwriting automation with their own Appcelerate program. This was designed for people who are in pretty healthy. If you can qualify, a life insurance policy can be issued by the next business day.

Read our full review of Banner

Founded in 1896, Fidelity Life is just one of the few life insurance carriers in the industry that has a focus on helping everyday Middle Americans experience life insurance ownership and the peace of mind that it brings. Fast forward to today. Fidelity Life is a life insurance company that is well capitalized. They are licensed to do business in every state except New York and Wyoming.

Fidelity Life has over $26 billion of life insurance in force. Fidelity Life understands that many families in America are competing daily with the economic pressures of life. Fidelity Life uses a patented technological system as well as innovative products in order to offer life insurance policies that are affordable and valuable to you.

Fidelity Life Tip – Using Fidelity Life’s digital tool, approval for life insurance happens at a much more rapid pace. Customers seeking insurance will not be required to give any kind of exam or oral questionnaire.

See our review for Fidelity Life

Gerber Life Insurance Company has been providing life insurance since 1967. Gerber has been providing life insurance options for young families with limited budgets for decades. Gerber Life Insurance is a separate affiliate of Gerber Products Company also known by most as “the baby food people.” These 2 companies have a common goal. That goal is to help moms and dads raise healthy, happy children.

Today, Gerber Life Insurance provides life insurance in the United States, Puerto Rico and Canada. Gerber Life has life insurance products available for a variety of age brackets and stages of life. Gerber Life has more than $45 billion of in force life insurance which provides financial security from over 3.3 million policies.

Gerber Life Tip – Gerber Life’s guaranteed issue is a great choice for those seeking life insurance who have been denied or may not qualify for other products.

Read our Gerber Review

Minnesota Life, also known as Securian, have been providing life insurance coverage since 1880. The Securian Financial Group is the holding company parent of Securian Life and Minnesota Life and its affiliates.

Minnesota Life focuses on what it takes to be successful, now and in the future.

Minnesota Life’s claims paying abilities and financial strength rank them among the highest rated life insurance company groups in the entire nation. Minnesota Life is consistent with their financial strength rankings and near the top by the four major independent rating agencies.

Minnesota Life Tip – Your medical history will be gathered via a telephone interview with Minnesota Life’s Non Medical Exam life product.

Learn more and read our Minnesota Life review

Mutual of Omaha can trace its roots all the way back to 1909. It was then known by the name Mutual Benefit Health and Accident Association. They filed their articles of incorporation with Nebraska Insurance Department.

Both United of Omaha Life Insurance Company and Mutual of Omaha Insurance Company display financial ratings that are strong from the industry’s 3 major independent rating services. These are A.M. Best, Moody’s and Standard & Poor’s

Mutual of Omaha is a Fortune 500 financial services and mutual insurance company. They are based out of Omaha, Nebraska. As a full service and multi line organization, Mutual of Omaha provides life insurance, financial products as well as banking products for individuals, businesses and groups. These services are provided throughout the United States of America.

Mutual of Omaha Tip – Your policy is renewable to age 100. This means you have the option of continuing coverage after the term ends up to age 100.

Learn more and read our Mutual of Omaha review

As a top life insurance and annuities provider, the North American Company for Life and Health Insurance has been around since 1886. They have fulfilled their commitments to their life insurance policy holders and customers.

Both families and businesses alike have counted on the North American Company to help out when times become challenging. They are there to help and assist during the difficult times as well as the good times ahead.

The North American Company has provided outstanding customer service, competitive life insurance as well as solutions for retirement for approximately 130 years.

North American has been solid with their financial strength and are committed to help their customers on the everything that matters the most to them.

North American Tip – The price breaks are at $100,000 and $250,000. So, let’s say you’ve done some figuring and determined you need $242,512 of coverage. If you round up to the $250,000 level, your policy might cost less per month.

Read our full review of North American Company

Phoenix Life started in 1851 and has always been about life insurance. This has been a focus and objective with Phoenix Life since they started.

Phoenix Life started in 1851 and has always been about life insurance. This has been a focus and objective with Phoenix Life since they started.

Phoenix Life provides products and services made to meed the financial needs of mass affluent markets and middle income markets. The goal of the Phoenix Safe Harbor Term Life and Term Life Express is to make and affordable term life insurance product for middle market customers.

Phoenix Life also wants to give you the added flexibility of living benefits. This will help you plan for the unexpected times and assist to protect your family and loved ones.

Phoenix Life Tip – Phoenix Life’s products have a focus on Living Benefits. If this is a major factor in choosing a policy, Phoenix Life must be considered.

Read our full Phoenix Life review

Beginning as an insurance company, Principal started in 1879. Now they are a member of the Fortune 500 as well as a global investment management leader.

Principal is a company that clients and advisors to to in order to reach their financial goals because of their support and solutions. Principal helps people make the kind of life that they dream about with stability and financial security.

Ranked number 3 overall for best overall service to micro plans, plan support, and value added advisor services. Principal has gotten the Adviser’s Choice Award for advisor support, post sale. Principal has also received more than 90 Best in Class designations over the past decade from PLANSPONSOR magazine’s Defined Contribution Services Survey.

Lastly, Principal has been named 1 of the World’s Most Ethical Companies as well as 1 of America’s Best Employers.

Principal Tip – Make sure you can qualify before you apply! Speak with your agent and they will pre qualify you so there are no surprises.

Read our full review of Principal

For over 175 years, Sagicor has built their business based on their long-term relationships with not only their employees, but with their customers and communities.

These are the important people who entrust Sagicor with their well being and financial future. Sagicor’s business strategy has been carefully constructed. Sagicor has been transformed a single line local life insurance company to a financial services group.

Sagicor now has a regional base that is solid and has expanded into the financial services market internationally. Sagicor’s financial stability has provided them with a solid reputation. This is because Sagicor’s reputation is based on their outstanding financial prudence. Since 1999, Sagicor’s excellent (A-) rating from A.M. Best Company has shown steady financial confidence.

Sagicor’s excellent rating is due to their financial strength and their ability to meet their ongoing obligations. Not only this, but also their operating effectiveness and strategic management.

Sagicor Tip – Sagicor uses a simple eApplication with Automated underwriting. A decision occurs in minutes (no telephone interview required).

Read our full review of Sagicor

SBLI started in 1907 and has been protecting more than a million families with dependable and affordable life insurance options. SBLI is consistently a low cost leader in the life insurance industry.

They offer some of the most affordable premiums in the country currently. These low rates are for both men and women. SBLI accomplishes this due to their excellent history of financial strength as well as SBLI’s prudent approach to investments.

A.M Best has been consistent with their ratings of SBLI. SBLI and their philosophy has consistently gotten the Superior (A+) rating from A.M. Best. This superior rating has occurred no matter the state of the economy.

SBLI Tip – SBLI has replaced the typical medical exam with a Telemed phone interview.

Read our full review of SBLI

In 1904, a young entrepreneur named Amadeo Giannini created the Bank of Italy in a converted San Francisco saloon. In 1928, Giannini merged with Bank of America, and in 1930 acquired Occidental Life Insurance Company through Transamerica Corporation.

Started in 1904, a young businessman named Amadeo Giannini started the Bank of Italy in San Francisco, California. Giannini then merged in 1928 with Bank of America. In 1930 the acquisition of Bank of Italy in San Francisco occurred.

Fast forward to today. Transamerica is committed to assisting consumers just as they did a century ago. Customers can now access an even larger range of financial services. Transamerica provides everything from retirement plans to life insurance in order to secure your financial future. Transamerica and their life insurance companies have all received excellent ratings for the most respected rating services in the industry – A.M. Best Company, Moody’s Investors Service, Fitch Ratings and S&P Global Rating Services.

Transamerica Tip – Transamerica offers their Terminal Illness Rider without an additional cost.

Read our full review of Transamerica

United Home Life’s website states that they keep the promises they’ve made to their policy owners for over 70 years. Their goal is to offer life insurance products that are easy to understand and that will give security to the ones you love.

United Home Life offers a variety of life insurance products including term, whole life, and accidental death coverage. Many of United Home Life’s plans can be custom made to meet specific life insurance goals with their additional benefits and riders. Several of which are at no-cost to you.

United Home Life offers a variety of life insurance products including term, whole life, and accidental death coverage. Many of United Home Life’s plans can be custom made to meet specific life insurance goals with their additional benefits and riders. Several of which are at no-cost to you.

United Home Life received an A- from A.M. Best. They are a leading independent analyst of the insurance industry since 1899. They also provided a financial strength rating of A (Excellent) to United Farm Family Life. These are the fourth and third highest ratings, respectively, out of 16 ratings. All of our companies combined have over $2 billion in assets, and over $20 billion in in-force life insurance policies. United Home Life is solidly positioned to meet the promises they have made.

United Home Life Tip – United Home Life appears to focus on the older age groups of 50 years or older for life insurance and burial insurance.

Read our full review of United Home Life

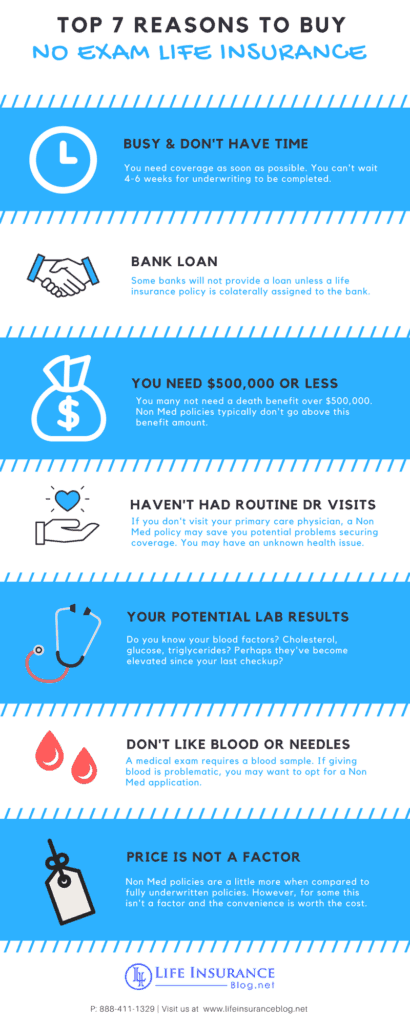

Getting a policy quickly is great, but many life insurance shoppers are concerned about their health.

For those who have been declined life insurance or are concerned about being denied, a non medical exam policy is very attractive. If you have a preexisting condition like high blood pressure, diabetes, sleep apnea, or high blood pressure – you may end up denied or with a very high premium.

Life insurance companies will consider you a high risk if you have certain health conditions or participate in high risk activities or occupations. These occupations and activities can reduce life expectancies. The simplicity of getting life insurance is the main benefit of securing term life without an exam.

Life insurance exams are time consuming and you may end up with a denial at the end of the underwriting process depending on how strict the life insurance company’s underwriting is.